Your subs have to provide qualifying insurance certificates and backup documents for you to approve, and whether you do this monthly or yearly, the back-and-forth trying to get all the proof you require is a killer. You have to read every document, check it against the rules, write back asking for a corrected COI or missing endorsement, and then chase down the response. Multiply by every contractor on every project.

Bex Insurance reads each certificate, endorsement letter, and policy document, and compares them to your specific requirements. If anything's missing or below standard, it proactively reaches out to subs, holding human-like conversations until the sub reaches full compliance. Your team stays in the loop—but doesn't have to bear the brunt of these rote activities.

Why insurance verification work is costly

Subcontractor insurance compliance is critical—but painful. Requirements like specific additional-insureds, waivers of subrogation, primary-and-noncontributory wording, and minimum coverage limits in multiple categories arrive in inconsistent formats from every broker. Or, the sub forgets to attach them. Reading a COI carefully takes minutes per document, and back-and-forth emails with subs cost even more time. Tracking who is actually compliant requires rote data maintenance. Spreadsheets get stale, overwrites from multiple employees cause errors, and frustration abounds.

Meanwhile the project moves on, and subs end up working without verified coverage because nobody had time to confirm. That kind of exposure compounds quietly.

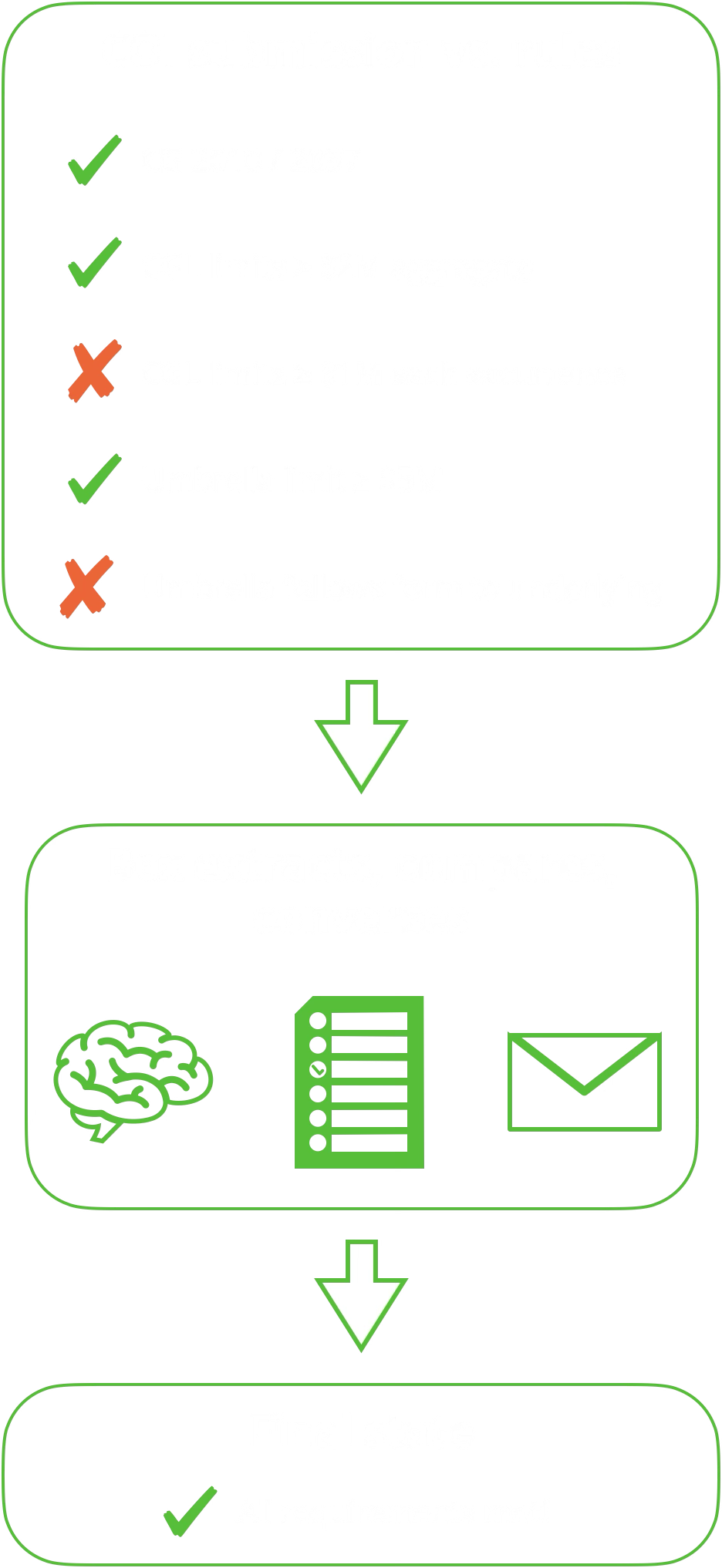

Where Bex comes in

When a COI arrives, Bex hashes and stores the document, reads it, and produces a Markdown assessment listing exactly which of your requirements are satisfied, which are not, and which are ambiguous. Each set of requirements is customer-specific, so the assessment is written in the wording, minimum limits, and endorsements you require.

If something is missing or unclear, Bex composes the follow-up email to the sub directly: "Your CGL shows $1M / $2M, but the project requires $2M / $4M with our entity named additional insured on a primary and noncontributory basis. Please provide an updated COI or a confirming endorsement." It reads like a note from a competent member of your team, not a templated form letter.

Where the human comes in

Most COI cycles are routine: a sub submits, Bex identifies the missing items, the sub provides them, and the sub is compliant. That entire cycle now happens without anyone on your side touching it. When Bex isn't sure (unusual policy structures, conflicting endorsements, incomprehensible replies from the sub), it escalates to your team with the relevant documents and its own analysis attached, so your team's time goes to the cases that actually need human judgment.

How Bex saves you time

- Your custom rules, configured in plain English.

- Direct conversation: Bex handles the back-and-forth with subs.

- Multi-document packets: COI, policies, and endorsements are handled together as one submission.

- Intelligent escalation: ambiguous cases reach a human; routine ones don't.